Nowhere is the convergence of public and private markets more evident than in semiliquid investment vehicles, a group that includes interval funds, tender-offer funds, nontraded business-development companies, and nontraded REITs.

To help investors understand and navigate these once-obscure but now rapidly growing investment options, Morningstar recently published The State of Semiliquid Funds, a report designed to help investors make informed decisions about them. Here, we share some of the key takeaways.

What Are Semiliquid Funds?

Semiliquid funds aim to make private markets more accessible—but they don’t always make them more affordable.

Semiliquid vehicles offer shareholders fewer opportunities to redeem shares than exchange-traded funds, which trade like all-day stocks, and mutual funds, which settle up once per day when the markets close. Investors in semiliquid vehicles can only withdraw their money periodically, such as quarterly or annually, and even then, the size of the withdrawals is usually capped.

At the furthest end of the vehicle liquidity spectrum are private partnership drawdown funds that lock up money for as much as a decade. They were historically the vehicle of choice for private capital managers, but now those managers are entering the semiliquid market aggressively, looking for new investors.

The 2025 semiliquid funds report focuses on US-based interval funds, tender-offer funds, nontraded BDCs, and nontraded REITs. For now, we’ve excluded European semiliquid structures.

What’s Driving the Growth of Semiliquid Funds?

Semiliquid vehicle assets grew to $344 billion at the end of 2024, up 60% from the end of 2022. Private credit has driven most of that growth, especially in nontraded BDCs and interval funds, which have grown the most in terms of both assets and fund numbers over the past three years.

The growth of credit-focused semiliquid vehicles makes sense. Public and private credit generate regular income, so payout-focused investors don’t need to withdraw capital to get what they’re seeking. This, in turn, takes some of the burden of managing withdrawals off asset managers.

While semiliquid vehicles that invest in real estate and infrastructure were the second-largest slice of the pie after credit, their market share has shrunk in the face of outflows in 2023 and 2024 and the growth of the other broad asset classes.

Private equity and venture capital, on the other hand, don’t generate regular income and are much more difficult to trade, which may account for their slower growth. These asset classes don’t work within the nontraded BDCs and nontraded REITs and are generally considered too illiquid for interval funds, which leaves tender-offer funds as the semiliquid vehicle of choice for private equity and venture capital.

Semiliquid Funds Have a High Bar to Clear

Costs are semiliquid funds’ Achilles’ heel: The average expense ratio for semiliquid vehicles was 3.16%, compared with a 0.97% average for active mutual funds and ETFs and a 0.37% average for passive mutual funds and ETFs.

Semiliquid fund managers need to clear a huge performance hurdle before the new investors they’re courting can consider these vehicles worth their trade-offs. Management fees tend to be higher, as do miscellaneous other fees, while some funds have substantial acquired fund fees, or fees paid to other underlying funds in their portfolios.

The 3.16% average expense ratio also includes incentive fees (also called performance fees), which many of these vehicles levy on either capital gains or income, so the hurdle is often even higher. Incentive fees charged on income are particularly pernicious because the hurdle rates and catch-up fees are structured so that funds always—barring extreme losses—earn their full incentive fees.

Additionally, only qualified clients, or those who meet certain minimums for net worth or investable assets, can invest in vehicles that charge incentive fees on capital gains, but there are no such restrictions for funds that charge incentive fees on income. So, there’s a risk that asset managers lure investors who don’t have the assets to absorb the costs, liquidity trade-offs, and risks of these offerings.

Many of these vehicles also employ leverage, or invest borrowed money, to boost returns. Leverage comes with additional costs that shareholders, not asset managers, bear. It can be profitable when managers earn higher returns than the cost of borrowing, but disastrous when they don’t, and there are conflicts. Managers can earn more by charging base fees on the money they borrow, and that leverage can help them clear hurdle rates that allow them to charge their incentive fees, even when the net results aren’t worth it for the client. The fee structure itself is an incentive to leverage up funds.

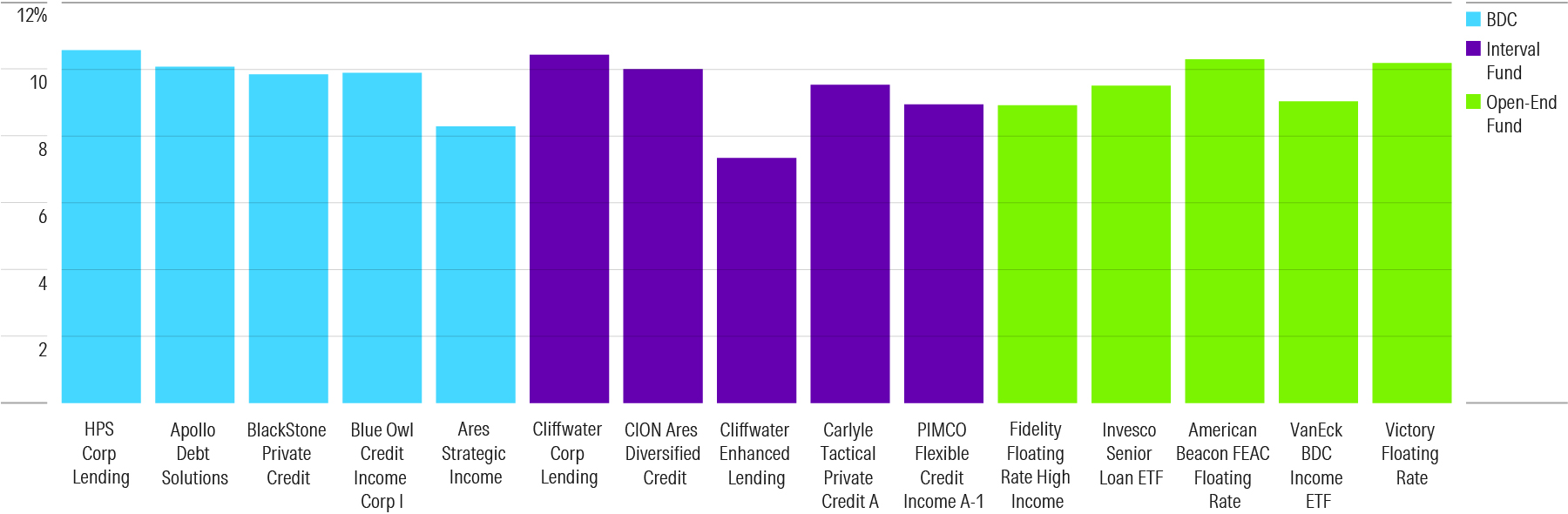

Is Performance or Leverage Behind Semiliquid Funds’ Returns?

Public and private credit vehicles employ leverage more than private equity funds. It has worked as intended, thus far: Many of the largest semiliquid credit funds have beaten the Morningstar LSTA Leveraged Loan Index. Those funds’ gross yields, or yields adjusted for leverage, however, are similar to those of open-end bank-loan funds. So, semiliquid funds’ excess returns appear to have come from leverage, rather than loan selection.

Meanwhile, the returns of semiliquid vehicles that invest in private equity have largely disappointed; most have failed to beat the S&P 500 since their respective inceptions.

3 Things to Remember About Semiliquid Funds

Asset managers are flooding investors and advisors with sales pitches for funds offering access to rarefied assets, like private equity and private credit. These vehicles’ complexity means remembering these investment truths is more important than ever:

- Costs matter.

- Shareholder-friendly practices will win in the end.

- Investors should be compensated for the risks they bear, including the liquidity they’re giving up.

That’s why Morningstar created a methodology for rating semiliquid funds and expects to launch initial ratings on a set of interval funds in the third quarter of 2025.

For those with access to Morningstar Direct, click here to view the Interval Fund Universe, and here to view the Tender-Offer Fund Universe.

link