Need to Know:

- Banks’ pandemic-era push to personalize messages improved engagement but didn’t meaningfully reduce deposit attrition because customers still chase higher yields, and competitors can easily copy marketing personalization.

- The “great deposit regression” reflects deposits flowing out of traditional bank products — especially savings and money market accounts — that fintech now makes easy to “rate-harvest” and into higher-yield, flexible alternatives like U.S. Treasuries.

- The durable fix isn’t better emails or apps alone; it’s deposit product customization (e.g., custom CD maturities, hybrid savings/CD structures, fair early-withdrawal terms, and daily CD market values) that matches how depositors actually want to save and invest.

Beginning in 2020, banking decided to embrace personalization. Fueled by societal separation during the COVID-19 pandemic, much of the industry discussion about engagement focused on how to deliver personalized messages at the right time, in the appropriate digital channel, and with the right content.

Helping people make informed decisions and feel more confident about their financial future is a worthwhile goal. But there’s one problem: Personalization does not appear to have made a dent in deposit attrition, nor did it overcome depositor desires for higher yields. A healthy portion of the industry invested in loyalty driven by personalization, but rising prices made its impact trivial. Instead of seeing deposit growth, the rollout of personalization corresponded with banks’ most significant deposit regression in their history.

Now, if you’re a banking executive, you likely read the above paragraph and thought, “Of course, nothing can keep a depositor from leaving if they just want the highest price, not even really effective messages.” If that describes you, read on; this article was written for you.

Personalized messaging has utility; it wasn’t a bad investment. But competitors can easily replicate it (fintechs were well ahead of banks in 2020 on this score), and thus it did not create durable differentiation. If banks want to retain and attract more deposits, they need to take personalization one step further: Personalize deposit products by customizing them.

Here’s why the data points to that conclusion, and how banks make product customization a reality.

What Great Deposit Regression?

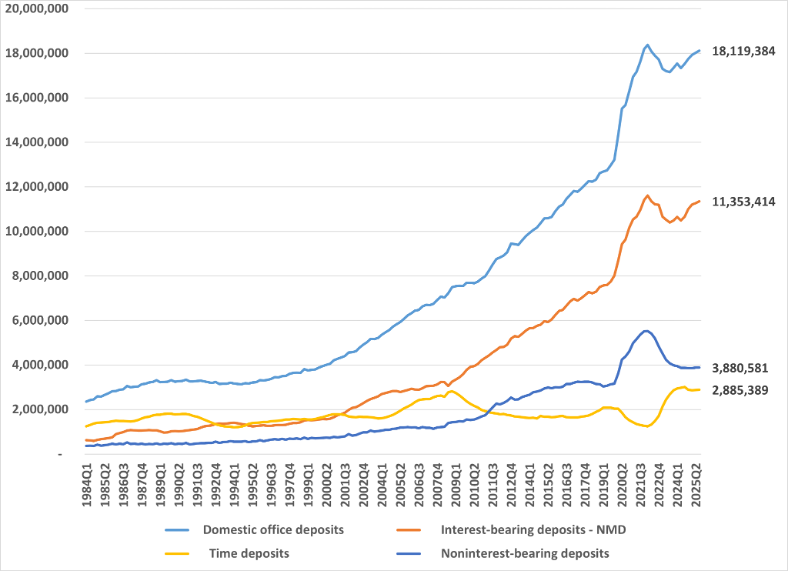

Are bank deposits in a regression? A picture illustrates better than words.

Looking back at pre-2021 bank data, total deposits grew every year. Even during the pre-pandemic rate increases, while volumes were indeed affected, total bank deposits still rose. That’s not so today. All types of bank deposits have now shown that they may not grow. Even the most popular deposit product (interest-bearing deposits, also known as savings accounts) has not regained its 2021 high point.

Chart showing banking’s great deposit regression.

The Financial Brand has covered each element of this regression during the past year for each color line on this chart: interest-bearing non-maturing (savings accounts and money markets); non-interest-bearing non-maturing (checking accounts and treasury accounts), and time deposits.

Savings accounts and money markets have become a flight risk because fintech now automates depositors’ ability to rate-harvest. Tools now warm no-commitment deposits to levels unknown when banks were cash flush and interest rates were at near-zero. Savings accounts are a lovely product for managing interest expense when institutions expect rates to decline – so long as the balances don’t depart when the bank drops the rate.

Before the age of fintech, a depositor had to decide to move their money, log in, and execute an order (at a minimum). Savings accounts were more likely to be sleeping money before. Now, they can become hot money instantaneously even while the depositor is sleeping.

Growth in new non-interest-bearing accounts (checking accounts) has been dominated recently by two of the nation’s leading fintechs. Together, their DDA growth rate has outpaced that of the country’s largest bank by a factor of two, according to J.D. Power’s “Financial Services Churn Data and Analytics” study of 80,000 U.S. consumers.

Certificates of deposit were the first to fall in volume as banking disruption set in after the Great Recession. Their rigid structure constrained banks and depositors alike, reducing their share of bank deposits. Many executives declared the death of the CD when all their deposit products could decline for the same reason: rigidity.

link