Theoretical framework and hypotheses development

The global accounting industry transforms with AI technology through efficient accuracy alongside automation benefits combined with fraud detection capabilities. Statistical evidence indicates developed economies have disproportionately adopted AI technology without fully understanding Saudi-Arabian markets affecting by the technology. An examination of AI technology showcases how it modifies financial processes and enhances accounting capabilities as well as raises fraud detection capacities and supports regulatory compliance measures while Saudi-Arabia executes Vision-2030 for its technological development. The paper offers workforce preparedness solutions alongside handling legal boundaries and moral issues. Saudi-Arabia’s distinctive characteristics receive complete analysis through the combination of TOE framework (Tornatzky and Klein 1982) and the KAP model. The TOE framework establishes a framework that integrates AI adoption through technological AI tool elements and anomaly detection algorithm implementation with organizational workforce training and organizational restructuring together with environmental regulatory policies and Vision-2030 objectives. The KAP model monitors how accountants’ AI knowledge together with their opinions about advantages and threats and their practical AI involvement determine the adoption results. The construct merges technological elements with human-focused components to bridge scholarly gaps about socio-technical complexities that generally remain unexamined in developing economies’ research.

The proposed hypotheses within this study adopt this theoretical framework to understand the effects these four elements have on AI adoption. The use of AI approximately twice per month enhances financial transaction operations by reducing human error rates and improving verification accuracy (H1) according to research found in invoice automation software examples (Zhou 2021). People who understand AI tools better will show increased capability in leveraging them (H2a) yet extensive automation dependence can cause workers to develop a sense of exhaustion (H2b) (Stancu and Dutescu 2021). Accounting professionals need systematic upskilling training programs because AI will play an essential role in their field (H3) according to Aljaaidi et al. (2023) and these established educational programs make workforce transitions more efficient. The implementation of AI technology requires additional interventions for effective improvements to take place. Transaction processing efficiency benefits from advanced automation technology only when supported by organizational policies and regulatory mechanisms (Wassie and Lakatos 2024; H4). AI delivers better accuracy and cost efficiency through proper strategic planning that connects technology applications to organizational targets (H5) (Seethamraju and Hecimovic 2022). Demographic attributes affect adoption patterns because women potentially experience different usability perceptions compared to men (H6) (Schweitzer 2024), professional workers with younger ages show higher engagement compared to their older colleagues (H7) (Abdullah and Almaqtari 2024) and professionals with higher education levels endorse AI integration (H8) (Teubner et al. 2023).

The implementation of organizational programs stands above AI use alone as the critical factor accounting professionals need for change readiness (H9) (Muspratt 2018). Professionals equipped with proper preparation create increased operational speed and lower operational costs together with heightened accuracy rates (H10) (Ballantine et al. 2024). Strong Results in fraud detection and enforcements require positive relationships between user engagement and outcomes to be successfully managed through AI awareness (H11) usage frequency (H12) and ethical governance (H13) according to Norori et al. (2021) and Alkhwaldi (2024). The study enhances AI adoption research by linking TOE and KAP frameworks to present a socio-technical viewpoint that rare in developing economies research. This theoretical contribution brings demographic factors (age, gender, education) as moderators with ethical concerns to enhance studies about equitable AI implementations. The analysis utilizes SEM provided by ADANCO for hypothesis validation while overcoming geographical sample bias challenges (Wassie and Lakatos 2024).

The successful deployment of Vision-2030 demands preparation of the workforce and explicit guidance linked to ethical management practices to accomplish AI adoption. In order to adopt AI successfully Saudi policymakers need to establish three fundamental strategies starting with training their citizens about AI fundamentals alongside offering platform incentives and regulating algorithmic discrimination and employment vulnerabilities (Lee et al. 2018; Schweitzer 2024). Organizations must make reskilling programs their highest priority through developing policies which will ensure innovation but maintain compliance regulations. The research develops a model to study AI adoption in developing economies by integrating global theoretical concepts with Saudi-Arabian context while illustrating how technology engages with human capital and government mechanisms. The national AI-driven accounting leadership aligns Saudi-Arabia to advance Vision-2030 sustainable economic transformation goals.

Research approach, sampling and data collection instrument

The research approach follows a quantitative method to study AI adoption in Saudi accounting practice while combining the TOE framework (Tornatzky and Klein, 1982) with the KAP model. Research adopts ADANCO as the structural equation modeling approach for analyzing survey data to perform hypothesis testing through composite-based analyses (Wassie and Lakatos 2024). The choice of ADANCO as modeling framework was motivated by its ability to handle formative constructs which includes AI engagement and regulatory influence thus being optimal for developing economy AI adoption research (Hair et al. 2021). The research methodology follows established standards of scientific rigor when used for SEM modeling in accounting and finance according to Silva et al. (2022) and Seethamraju and Hecimovic (2022).

A questionnaire survey targeting 101 Saudi accounting academics was conducted between February and March of 2024 through a university network and professional connections. Academics forming the majority of participants represent a workforce with extensive knowledge of accounting education and auditing and financial reporting hence their insights are suitable for examining both educational and industrial concerns (Alharasis 2024; Ballantine et al. 2024). Academic participants selected for this survey represent Saudi-Arabia’s technology-driven populace that directly supports Vision-2030’s human capital development goals as identified by Duan et al. (2019). Research indicates that survey participants included 65% males and 36% people aged 25–34 together with 47% holding doctoral degrees thus manifesting their preparedness for AI implementation in their academic domain. Saudi accounting scholars contribute essential analysis about academic concepts and practical issues in ambiguous regulations which addresses educational requirements and compliance standards (Hamza et al. 2024; Schweitzer 2024). The research used Mgammal (2024) questionnaire adaptation as a self-administered instrument to measure AI adoption in accounting per previous research by Bygren (2016), Li and Zheng (2018), Afroze and Aulad (2020), Rashwan and Alhelou (2020), Akinadewo (2021), Al-Rifai (2022), Assaf (2022), Qhabeel et al. (2022) and Aljaaidi et al. (2023). The initial five queries in the survey collected respondent data that included age, gender, education status along with professional accounting tenure and organizational affiliation type. The survey design incorporated representative sampling methods for various experience levels which generated extensive knowledge regarding Saudi-Arabia’s accounting profession’s AI adoption scope.

Supplementary Appendix 1 included a structured questionnaire that achieved both convergent validity with AVE above 0.5 as well as discriminant validity through Fornell-Larcker criterion. The study measured key variables which include frequency of AI system usage together with organizational familiarity about AI technologies and their financial transaction processes and their readiness for organizational changes. AI usage frequency assessment relies on tracking how often respondents use AI tools such as ChatGPT and fraud detection algorithms in their accounting workaday (Zhou 2021). AI familiarity functions as a tool to assess employee understanding about technologies that use AI capabilities alongside their perception of associated risks as described by Stancu and Dutescu (2021). Financial transaction processes concentrate on enhancing transaction precision as well as detecting fraudulent activities because they directly serve financial reporting compliance standards worldwide (Puthukulam et al. 2021). The measurement of change preparation emphasizes workplace readiness through technological programs because of existing research investigating accounting personnel adaptability (Aljaaidi et al. 2023 and Mgammal 2024).

The reliability test followed Cronbach’s alpha (>0.7) measurement while bootstrapping through 5,000 resample sets maintained the stability of parameter values (Hair et al. 2021). Each empirical construct received specific adaptation to fit Saudi-Arabia’s regulatory framework that supports both Vision-2030 AI governance policies and IFRS compliance (Zhou 2021; Wassie and Lakatos 2024).

This study employs ADANCO for composite-based SEM, rather than covariance-based SEM (CB-SEM), due to several methodological considerations. ADANCO demonstrates outstanding suitability for emerging technology analysis within developing economies because it supports both predictive studies and new technology trend examinations (Wassie and Lakatos 2024). ADANCO offers support for formative constructs with composite modeling since AI engagement and ethical governance constructs need approaches beyond reflective modeling of CB-SEM (Hair et al. 2021). ADANCO offers effective analysis of smaller dataset populations especially for Saudi accounting scholars whereas CB-SEM needs larger sample sizes according to Silva et al. (2022). The study investigates age and education variables as moderators because they integrate well with ADANCO’s sophisticated multi-level connection modeling capabilities (Norori et al. 2021). Meanwhile, AI awareness works as a mediator which ADANCO also supports through its advanced relationship modeling (Norori et al. 2021).

The use of covariance-based SEM mainly supports theory confirmation through assessment of goodness-of-fit indices like CFI and RMSEA. The model should be selected as the most suitable fit for research that needs to determine essential factors behind AI adoption since it maximizes variance explained through its R² values. The composite-based SEM analysis conducted by ADANCO demonstrates that accounting efficiency depends on 92.35% of variables (H10), thus confirming the significance of AI training and workforce preparation for AI adoption patterns (Ballantine et al. 2024). Researchers support AI literacy programs to prevent job loss and improve automated financial reporting according to Muspratt (2018) as well as Lee et al. (2018).

The methodology decisions from the study hold important practical consequences. The goal of maximizing variance explanation (R²) within ADANCO helps policymakers and business leaders create specific AI literacy programs and regulatory policies that produce better adoption results (Luo et al. 2018). The study confirms H6 and H7 to provide demographic evidence which benefits the creation of inclusive AI teaching plans (Schweitzer 2024; Abdullah and Almaqtari 2024). The study reveals that automation fatigue exists because excessive AI usage leads to disengagement according to the negative coefficient in H2b. AI governance frameworks must establish systems to manage technological progress against workforce health because Stancu and Dutescu (2021) highlight this need.

ADANCO’s composite-based SEM methodology enables this study to conduct a strong analysis of AI adoption in Saudi-Arabian accounting which complies with international best practices while supporting Vision-2030’s digital transformation initiatives. The research demonstrates that educational institutions serve as essential components for developing an AI-competent workforce and uncovers how AI boosts fraud identification together with financial effectiveness and automatization abilities in various industries (Zhou 2021; Teubner et al. 2023).

The study provides comprehensive findings about AI usage by Saudi-Arabian accounting academics but additional research should examine implementation strategies of AI technology in private sector companies with professionals. The research framework from this study provides a reference point for future developing economies AI adoption investigations because it demonstrates the three-point connection between technology, governance, and human capital (Mgammal 2024).

Diagnostic tests

Reliability

The measurement meant the use of numbers, percentages, means, and standard deviations for the closed-ended responses from the participants. Content analysis of the responses was also used to derive themes regarding the limitations of AI and areas of preparation. Cronbach’s alpha reliability coefficients were used to test the internal consistency of the Likert-scale measures. It also made it possible to consider whether the data obtained through the questionnaire could be credible for identifying accountants’ perceptions of the usefulness of AI within the profession. All reported items are presented in Supplementary Appendix 1.

Data collection method

The target population in this study was academics in the field of accounting in Saudi-Arabia, and the technique adopted for sample selection was snowball sampling. Google Forms was used to generate a link through which the respondents could access the surveys sent to them. Considering the target audience, the link to the survey was personally sent to the academics in the field of accounting by the researchers through their working email addresses and through the social media sites: WhatsApp groups, Instagram accounts, Snapchat, Facebook, and the ‘X’ platform where the researchers directly tagged the SOCPA account and appealed for the account followers to help the researchers in data collection. This survey was conducted between February and March 2024, and data collection was also conducted within this time frame. In total, 101 specialists completed the questionnaires.

Data analysis

To test the hypothesized research model, we employed ADANCO, an approach to CA-SEM. Based on Anderson and Gerbing’s (1988) recommended two-step approach, the first step involved the assessment of the measurement model for the construct under study; that is, employability skills using confirmatory factor analysis (CFA) to establish the validity and reliability of the construct. We then further evaluated the structural model employing the techniques provided by Hair et al. (2021) to analyze the hypothesized relationships among the constructs. A covariate multiple regression equation with OLS estimation was employed to estimate awareness, usage, engagement, and demographics as antecedents of financial processes, change preparedness, and accounting efficiency. Furthermore, a binary logistic regression test was performed to analyze the impact of the independent variables on the binary perceived positive impact of the AI-dependent variable. A set of CFA tests was employed to check the convergent and discriminant validity of the measurement models. While CFA was applied to estimate the measurement model, other hypotheses were tested using OLS regression, while binary outcome hypothesis testing was performed using logistic regression. In line with the two-step CFA procedure to validate the measures and structural modeling procedure for survey-based research models, the procedure meets the standards.

Models

We employed two types of regression models: simple linear regression, multiple regression, and logistic regression. OLS Regression is a linear regression technique that measures the relationship between dependent and independent variables and calculates the degree of variation between the dependent and independent variables’ predictions. It was used to determine the coefficient of the independent variables; awareness, usage, engagement, demographics and dependent variables such as ‘Financial Transaction Processes,’ ‘Preparation for Change,’ and ‘Accounting Efficiency, Accuracy and Costs.’ Logistic regression is used when the dependent variable is nominal, and it models the probability of a certain input point belonging to a certain category. This model was applied to determine the binary dependent variable of perceived AI impact, which was established based on the average of the questions regarding the effectiveness of the use of AI in the organization. Particularly, hypotheses numbers one through ten related to the use of the continuous dependent variable used the OLS Regression method, while the binary outcome analysis to categorize respondents’ perception about AI happened with the help of the Logistic Regression method.

Survey data analysis

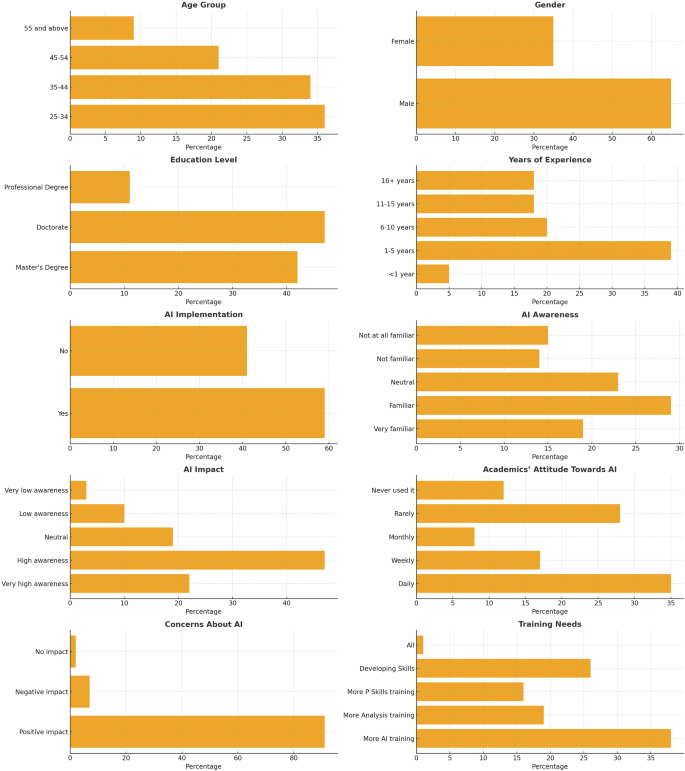

In Fig. 1 and Table 1, we see that what came out from the data is an overview of a relatively large, mostly male (65%), fairly youthful (36% being 25–34 years of age), and educated group (47% with doctorate’s degree, 42% with master), which is reflective of a progressive and wise group. A majority of the respondents had been in the field for less than five years (39%). AI implementation is still growing, with 59 percent of entities reporting their implementation of AI applications; this combined with high levels of awareness, with 48% (19% + 29%) of the respondents being very familiar or familiar with AI. The daily usage of AI is moderately high (35%), signifying that the usage of AI technology in daily activities is on the rise, but the remaining 28% uses AI very sparingly. At 91%, the level of acceptability of AI’s influence indicates optimism; thus, the growth and development of AI is expected in the future. The variation in the training requirements, which extends to areas such as AI (38%) and skill upgrades (26%), shows an audience who is willing to learn more. Thus, further strengthening of AI’s presence, promotion of its application, and support of targeted training should be viewed as a continued enhancement of this promising groundwork toward developing more innovations with an emphasis on inclusiveness.

Age Group: Distribution of respondents by age categories. Gender: Gender distribution. Education Level: Distribution of respondents by level of education. Years of Experience: Distribution of respondents by experience. AI Implementation: Distribution of respondents by using of AI. AI Awareness: Distribution of respondents by Awareness levels of AI. AI Impact: Distribution of respondents by impact of AI. Academics’ Attitude Towards AI: Distribution of respondents by Academics’ Attitude. Concerns About AI: Distribution of respondents by level of Concerns About AI. Training Needs: Distribution of respondents by Needs of AI training.

Descriptive analysis

In Table 2, the data elicited provide insight into respondents’ attitudes and perceptions towards aspects of AI within the workplace. These demographic statistics reveal that the study participants’ age is relatively evenly spread with a mean age of 2.31 a standard deviation of 1.13, and that it can be slightly shifted to one side. Levels of education and experience are heterogeneous, with the median values of the tested variables being above average. Respondents’ perception and understanding of the usage of AI is positive, and the mean values show that they perceive the use of AI in their roles as helpful. However, the ranges defined by standard deviations speak of diversity and help measure differences in people’s experiences and attitudes. In this regard, the mean scores for AI efficiency, accuracy, and cost indicate a relatively positive attitude toward AI’s effects on professional productivity and financial knowledge, albeit with certain concerns. Another variable that has improved is trust in AI, where the trend is also on the rise, although the std reveals that there is a possibility of increasing confidence slightly. Accounting and the role of AI, as well as weaknesses and training needs, imply a closer look at the insights, which, on the one hand, reveal high regard for AI, and on the other, its further development and education. In conclusion, it can be said that people have a rather optimistic attitude towards AI, although it is accompanied by a desire for further development of knowledge and trust in the subject. This critical analysis also insists on the reduction of variability in the experiences of AI and the concentration on proper training of the AI system to achieve enhanced results.

Measurement of the model

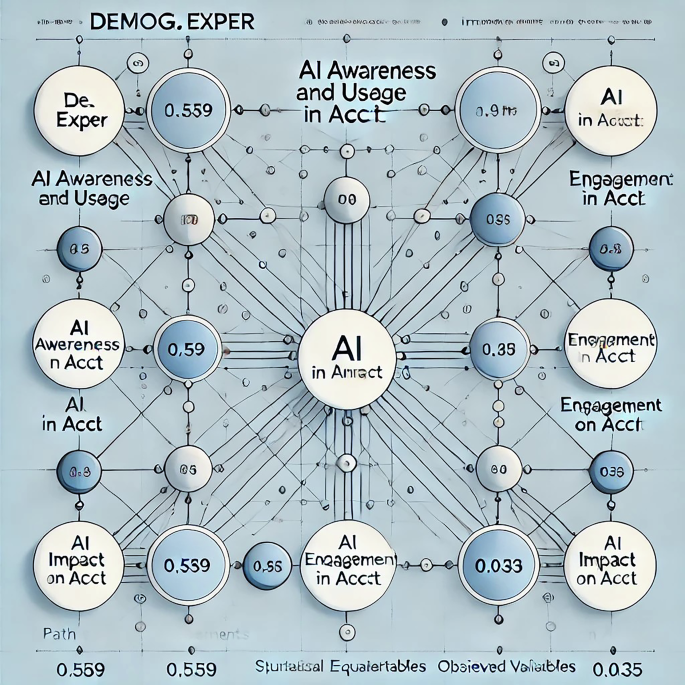

In Fig. 2 below, the SEM diagram represents the relationships between several key factors related to AI’s impact on accounting. It shows how demographics, AI awareness and usage, and AI engagement contribute to the impact of AI on accounting outcomes such as efficiency, accuracy, and costs. Path coefficients (like 0.559) indicate the strength of these relationships, with arrows showing the direction of influence. The central latent variable, AI Impact on Accounting, is influenced by factors like AI engagement and demographics, highlighting how various elements work together to affect accounting processes. The model helps visualize how these factors interconnect to shape the overall effect of AI in the accounting field.

The figure validates the structure of the proposed model, demonstrating how demographic and behavioral factors align with the effective use and impact of AI in accounting practicesFootnote

We use AI to produce the image

.

Convergent validity analysis

Based on Table 3, which shows the AVE and CR values for each construct, the AVE values for all constructs are 1.0, but it makes sense because all convergent validity refers to the extent to which each construct accounts for the variance of its indicators, and in this case, they all account for 100% of the variance. The CR values varied between 0.882 and 0.995, which also indicates its high performance, where the minimum CR must be 0.7. This indicates that all the constructs have good-to-excellent internal consistency reliability, as depicted below. More specifically, CR values that indicated superb reliability were above 0.99 for the financial transaction processes, preparation for change, and accounting efficiency/accuracy/cost factors. – Among all the constructs, the lowest CR value was found in the AI Usage construct with a value of 0.882; however, it is relatively reliable, with values above the standard cut-off. In summary, both AVE and CR values reveal that the measurement model demonstrates high levels of convergent validity and internal consistency. The constructs are dependable and have validity with reference to their conceived ideas.

Discriminant validity analysis

Fornell, Larcker (1981)

The square root of the AVE for each construct in Table 4 is greater than the correlations with the other constructs, indicating good discriminant validity.

Table 5 results show that the items generally load higher on their respective constructs than on others, indicating good discriminant validity.

Correlation analysis

Table 6 shows that several multiple variables are evidently related in the given dataset. Looking at the correlation between age and experience it is apparent that the relationship between them is at 0.804 which can be regarded as rather high This means that the older people are, the more work experience they are expected to possess. Gender and AI usage are also closely related with a correlation value of 0.837, which implies a moderate level of relationship between the two. The results of correlation analysis show that there is a negative correlation between AI degree and repetitive AI control (−0.702); It indicates that greater application of AI is likely to mean that it is used less repetitively, possibly because it is used more effectively. Thus, perceived opportunities and constraints of AI (0.705) appear to have a positive linear relationship, meaning that as people’s perception of the opportunities created by AI expands, so does their estimate of the constraints. The perceived effectiveness and accuracy of AI are positively related to encouragement for analysis as well as usage in accounts (0.773, 0.719 respectively) suggesting that efficient AI tools encourage more analytical initiatives and gateways into proceedings in accounts. Respondents that were encouraged to understand the financials of a business were more inclined to be encouraged to perform an analysis as well as utilize AI in accounts hence the correlation coefficient of 0.733 for this statement and 0.754 for this statement. Also, trust in AI is strongly correlated with accounts’ AI usage (r = 0.826), which confirms the hypothesis that increased AI trust results in increased AI integration in accounts.

We use AI to produce the image

.

link