The impact of digital inclusive finance on enterprise digital technology innovation: empirical evidence from the Chinese manufacturing industry

Digital inclusive finance and enterprise digital technology innovation

Digital inclusive finance represents an innovative financial approach that integrates traditional services with cutting-edge digital technologies. Its core objective is to expand financial service access by reducing entry barriers, lowering transaction costs, and enhancing service availability. According to the resource-based view (RBV) theory (Barney 2001), digital inclusive finance constitutes a valuable, scarce, and non-replicable asset, enabling firms to secure sustainable competitive advantages through technological advancements. By enhancing financial service accessibility—owing to reduced market entry barriers and lower transaction costs—digital inclusive finance facilitates more efficient acquisition and utilization of financial resources, thereby fostering digital transformation and enterprise innovation. The unique attributes of this resource allow firms that effectively leverage digital inclusive finance to achieve superior market competitiveness.

Information Processing Theory underscores how organizations process and react to external information (Yadav et al. 2024). Digital inclusive finance improves the efficiency of both internal and external oversight by mitigating information asymmetry. This enhanced transparency builds trust between stakeholders and enterprises, strengthens internal controls, and creates a conducive environment for decision-making and operations during the digitalization process. Leveraging technologies such as blockchain, big data, and cloud computing, digital inclusive finance increases information transparency and regulatory effectiveness, addressing issues like equity dilution, commercial bribery, and illegal disclosure while significantly reducing agency costs (Lu and Cheng 2024a).

Innovation diffusion theory describes the spread of new ideas, behaviors, and products throughout society. As an innovative financial service model, digital inclusive finance attracts social capital through digital platforms, reduces marginal costs associated with market development and financial operations, lowers information collection and user conversion costs, and eliminates financing barriers, thus promoting direct financing (Zhang et al. 2024). It not only reflects the scale and long-tail effects of the financial market but also caters to diverse market demands, providing financial support for various enterprises engaged in digital technology innovation. The advancement of digitalization helps enterprises overcome psychological barriers when accessing financial services and alleviates issues such as price exclusion, market exclusion, and self-exclusion. Additionally, the widespread adoption of digital technology encourages enterprises to explore new business models and service methods to maintain competitiveness, accelerating the pace of digital technology innovation and application.

In conclusion, digital inclusive finance not only enhances enterprises’ ability to secure funds through more transparent and efficient financial services but also stimulates innovation activities by reducing transaction costs and improving capital accessibility. This dual effect promotes high-quality economic development at both macro and micro levels.

Based on these insights, this paper proposes Hypothesis 1: All other things being equal, there is a positive impact of digital inclusive finance on corporate digital technology innovation.

Transmission mechanism: the intermediary role of financing constraints and R&D investment

Digital inclusive finance may influence enterprise digital technology innovation in two potential ways: financing constraints and R&D investment.

Financing constraints, as a form of market friction, theoretically limit enterprises’ reliance on external funds. Given that China’s financial market is still in its developmental stage, the financial system remains imperfect, with deficiencies in the credit market and issues such as poor corporate credit records or insufficient transparency of financial information (Yao and Long 2024). Consequently, the financial system struggles to meet the financing needs of private small and medium-sized enterprises (SMEs), exacerbating the Macmillan Gap (Wang 2023). In this context of constrained financing, enterprises face limitations in their investment capacity, which directly impacts their ability to undertake long-term and highly uncertain digital technology innovation projects. The current status of ongoing projects becomes at risk when organizations decide to terminate them after implementation has started. The theory of agency predicts management during times of financing constraints may give up innovation projects with positive net present value (NPV) because of short-term interests, thus worsening investor conflicts and agency costs.

However, advancements in digital inclusive finance present viable solutions to these financial limitations. Digital inclusive finance decreases expenses related to finance and enhances the availability of financial services, thus helping companies manage risks linked to digital technology innovation projects. Through digital inclusive finance, financial institutions can evaluate a company’s credit risk precisely and enhance credit extension to a large extent (Mali and Yeboxia 2020). Flexibility in repayment or financial products with flexibility in financial burdens during the R&D and technology conversion phases is able to be devised on one hand by financial institutions for enterprise cash flow unpredictability. However, digital inclusive finance provides other sources of funding and lower financing rates that are more suitable for businesses’ particular financing needs and cash flow requirements. It is important to relieve the external financing constraints of an enterprise during its growth stage and boost its digital technology innovation capability. With the quicker pace of digital technology advancement, businesses must keep increasing the pace in applying new technological or digital advancements. Digital inclusive finance is a catalyst for this adaptation, based on the availability of the required funding. The funds allocated by enterprises for new technology investments, human capital development, and streamlining the innovation process help them gain an edge in the fierce competition in the market.

Based on this, this paper proposes Hypothesis 2a: All else being equal, digital inclusive finance promotes corporate digital technology innovation by alleviating financing constraints.

The R&D investment plays a crucial role in enhancing enterprise innovation and high-quality development. Excess returns and favorable signals can be produced by enterprises through R&D activities and strengthen enterprise value. However, investment in R&D often faces challenges such as high asset specificity, information asymmetry, uncertain outcomes, and mismatches between investment returns, which often lead to agency problems and increased credit risk for enterprises (O Connell et al. 2022). Additionally, the lack of funding, inefficient management, and malfunctioning market systems are frequent hindrances to innovation (Sun et al. 2024). Nevertheless, the advent of digital inclusive finance has adopted traditional financial services broader than ever before, and the latter has also offered fresh ways to tackle challenges.

In the first place, digital inclusive finance leverages informatization and big data technology to reduce costs of financing and lower the barriers to accessing financial services (Peng et al. 2024), and enables enterprises to allocate capital with more agility and lower risks associated with asset specificity. Second, digital inclusive finance advances digital technological innovation through the application of technologies such as cloud computing, big data, and the mobile internet, which increase the quality and speed of digital technological innovation. Taking advantage of information asymmetry, the problem of information asymmetry is resolved through the establishment of risk control and information monitoring frameworks that help financial institutions grasp a complete understanding of business scenarios (Guo et al. 2024). Moreover, digital inclusive finance brings professional evaluation institutions and models, which provide a more accurate matching between project risks and financial resources. In addition to that, this approach also provides a comprehensive analysis of the market prospects and technological feasibility of R&D projects and consequently reduces the impact of output uncertainty. Financial institutions can offer customized investment solutions and risk-sharing mechanisms to investors and enterprises to share the returns of investment more fairly. Thus, it increases investor confidence and induces more R&D investment (Ayaz et al. 2025).

Furthermore, digital inclusive finance provides solutions to fill the funding gaps and rejuvenate or even improve the innovation framework of the high-tech manufacturing sectors, especially when external economic disruptions strike them. It also facilitates information dissemination and collaborative efforts, enabling R&D teams to operate more efficiently. By leveraging contemporary financial instruments such as digital payments and fintech solutions, business operators not only increase their willingness to engage in innovative activities but also significantly boost their R&D expenditures, thereby fostering technological advancements and product evolution. In essence, digital inclusive finance enhances R&D investments for enterprises through more effective financial services, ultimately stimulating innovation in digital technologies.

Based on this, this paper proposes Hypothesis 2b: All else being equal, digital inclusive finance promotes enterprises’ digital technological innovation by increasing R&D investment.

Boundary effect: the regulatory effect of executives with financial backgrounds and the intensity of financial regulation

Since the characteristics and experience of the executive team can significantly influence a firm’s strategic choices, executives with a financial background may prioritize financial performance and the stability of traditional financial instruments based on their expertise and cognitive patterns (Li and Kong 2024). From the perspective of agency theory, managers possess control over corporate resources, and the constraints imposed by owners on their behavior may be limited. While traditional theories tend to view managers as fully rational “Economic Man” who act according to the principle of expected utility maximization and Bayesian learning, existing research has shown that corporate executives often exhibit short-sightedness in their economic activities, which can crowd out corporate governance and investment in innovation (Liu et al. 2020).

First, executives with a financial background may exhibit a preference for short-term financial outcomes and neglect long-term strategic planning. Due to loss aversion, they may reduce investment in digital technology innovation while pursuing financial stability (Gu 2023). There are many advantages of these executives’ financial expertise, such as overcoming the firms’ financing constraints and offering strong financial support, but at the cost of long-term nonfinancial performance.

Second, executives with a financial background may be more likely to rely on traditional financial resources rather than innovating resources from the digital technological field, which may restrict the firm’s expansion in the digital field. Therefore, while executives with financial backgrounds can provide a financial prop for firms, they may reduce the motivational effect of digital inclusive finance on firms’ digital technological innovations.

Furthermore, research in behavioral finance shows that managers have characteristics of limited rationality and that overconfident managers prefer endogenous financing over exogenous financing (Agha and Pramathevan 2023). This means that executives with financial backgrounds are likely to keep the cash inside the firm and reduce cash dividends. Such preferences can result in reduced investment in digital technology innovations, thereby limiting firms’ growth in the digital space.

Based on this, this paper proposes Hypothesis 3a: All other things being equal, an executive’s financial background diminishes the role of digital inclusive finance in promoting firms’ digital technological innovation.

As such, the dilemma associated with the tradeoff between financial efficiency and security is increasingly prominent following the occurrence of phenomena including P2P unraveling, users information leakage, platform monopolization, and data misuse (Xu et al. 2023b). The complexity, endogeneity, and volatility of digital inclusive finance have exacerbated the inadequacy of current regulation; that is, there is no single approach that would fit all the challenges of digital inclusive finance. fintech and digital finance that is inappropriate for financial regulation may hinder enterprise innovation with limited development and efficacy of fintech and digital finance due to the financial regulatory reform lagging behind (Ren et al. 2024). Consequently, the direction and degree of financial regulation are important for the formation of digital inclusive finance and can directly affect the development of different financial industries.

To effectively reduce financial market arbitrage, prevent and resolve liquidity risks, and support the healthy and orderly development of digital inclusive finance that better serves the real economy, moderate financial regulation can provide a stable policy environment for its growth (Xuan et al. 2024). This level of regulation successfully addresses traditional financial sector problems, promotes digital technological innovation in businesses, and aids in creating a standardized and orderly financial sector. Furthermore, prudent and effective financial regulations can enhance the targeting and security of digital inclusive finance, facilitate the precise provision of digital financial products, and mitigate micro-risks like credit and liquidity. This, in turn, increases the accessibility and depth of digital finance utilization for businesses (Qi and Sun 2024).

However, when the intensity of financial regulation exceeds a certain threshold, its detrimental impacts start to show. Overly stringent regulation may decrease incentives for innovation, raise compliance costs for businesses, and restrict the potential for innovation in digital inclusive finance. Moreover, overly stringent regulations risk undermining market competition mechanisms, stifling business innovation, and causing innovative digital inclusive financial products to disappear from the market, thereby impeding the advancement of enterprises’ digital technological innovation.

Therefore, this paper proposes Hypothesis 3b: All else being equal, the intensity of financial regulation produces an inverted U-shaped moderating effect between digital inclusive finance and firms’ digital technological innovation.

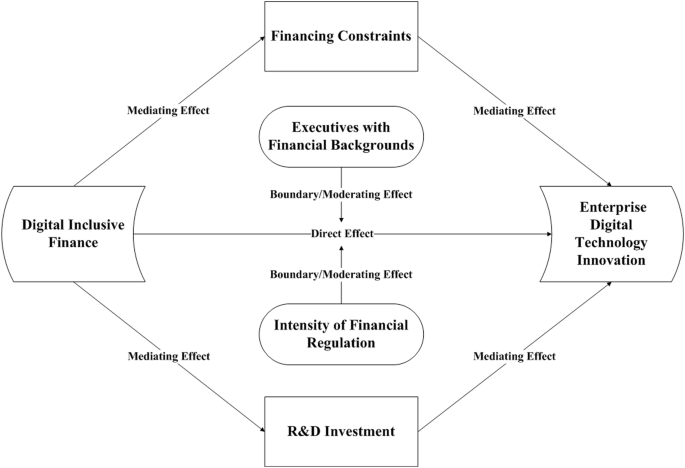

Based on the above research assumptions, the theoretical model of this paper is shown in Fig. 1.

link

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DZEDEORGTFD3LHOHW53OJBRLIU.jpg "Blue Owl Offers a Harsh Lesson for Semiliquid Fund Investors")